The Chennai real estate market in 2026 is moving through a phase that many buyers find difficult to interpret. On one side, there are clear signs of slowing demand. On the other, property prices continue to rise instead of correcting. This creates a situation where traditional assumptions about the market no longer apply in a straightforward way.

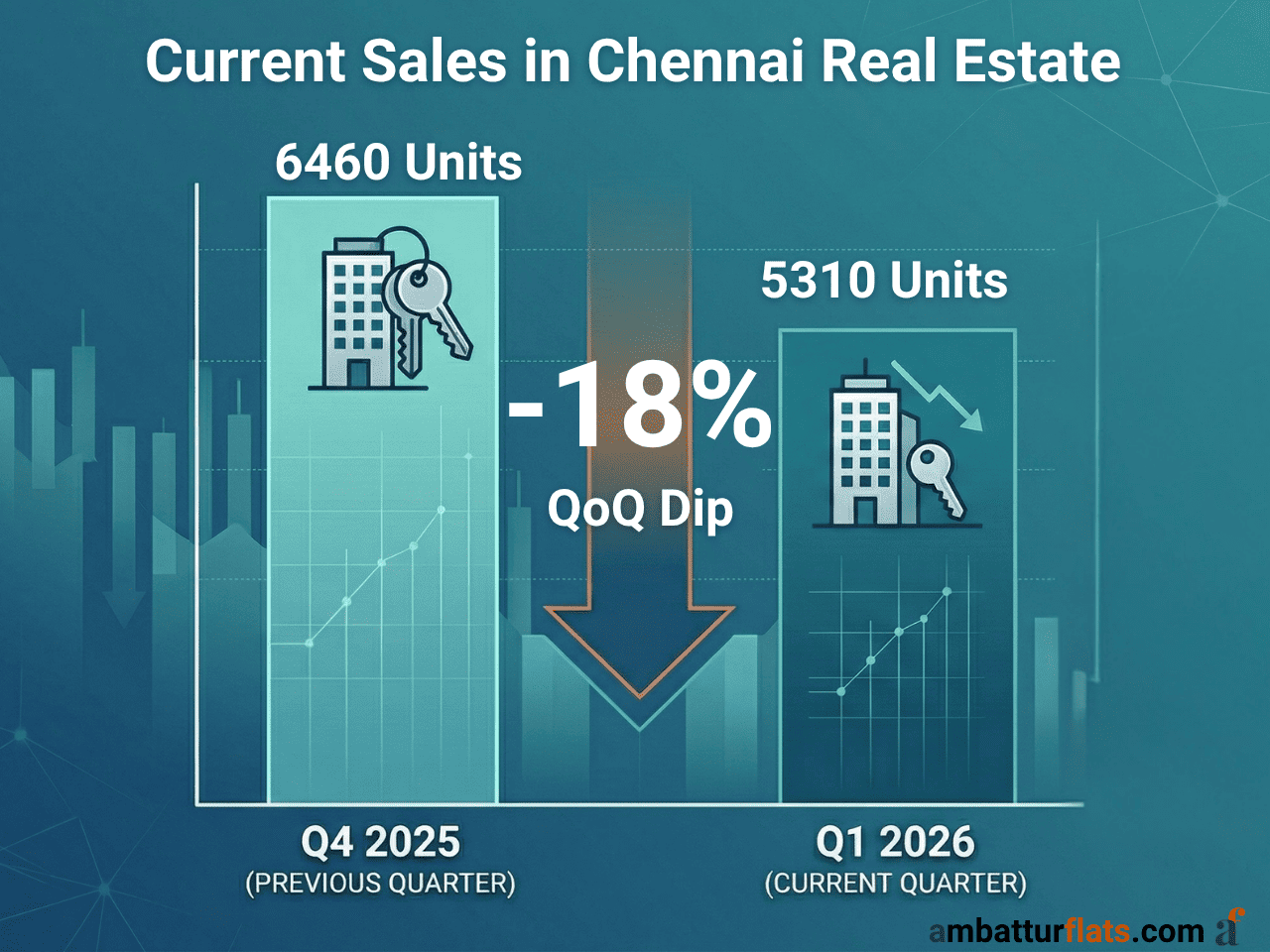

Recent data shows that housing sales across the top seven cities in India declined by about 7% in the first quarter of 2026 compared to the previous quarter. A drop in sales usually suggests weakening demand, but the absence of a price correction indicates that the supply side is behaving differently. For homebuyers, this is not just a market update. It is a shift that directly affects how buying decisions should be made.

To understand what is happening, it is necessary to look beyond a single data point. The slowdown in sales is not limited to Chennai alone. Across major cities, approximately 1,01,675 units were sold in Q1 2026, compared to around 1,08,970 units in the previous quarter. This indicates a broader reduction in transaction activity.

At the same time, the number of new project launches has not slowed down at the same pace. In fact, new supply has continued to enter the market, and in some cities it has even increased. This has led to a rise in unsold inventory, which has now crossed 6 lakh units across the top cities.

This creates a situation where supply is gradually building up while demand is temporarily slowing. Under normal conditions, such a mismatch would lead to price corrections. However, that has not happened in a meaningful way.

The reason lies in how developers respond to market pressure. Instead of reducing prices immediately, most developers prefer to hold inventory and wait for demand to recover. This is especially true in cities like Chennai, where land cost, approval timelines, and construction expenses create a strong cost base that limits how much prices can be reduced.

As a result, the current market is not a falling market. It is a slow-moving market, where transactions have reduced but price expectations remain firm.

The slowdown is driven by a combination of external and internal factors rather than a single structural issue.

One of the primary reasons is global uncertainty. Geopolitical tensions have affected economic sentiment across multiple sectors. In real estate, this does not immediately reduce demand, but it delays decision-making. Buyers tend to postpone large financial commitments when uncertainty increases. According to market observations, even international investors, particularly those from regions directly affected by global tensions, have slowed down their activity .

Another important factor is the rise in construction costs. Increases in fuel prices have a cascading effect on materials such as cement, steel, and transportation. Developers who are already operating with tight margins are not in a position to reduce prices significantly. Instead, they pass on part of the cost pressure to buyers or hold prices steady.

At the same time, buyer expectations are playing a role. Many potential buyers are waiting for a correction that may not occur in the way they expect. This waiting behavior reduces transaction volume even when affordability has not changed drastically.

The combination of these factors results in a temporary slowdown in activity without triggering a sharp price decline.

For homebuyers, this phase requires a different approach compared to a high-demand market. The key difference is that the pressure to make quick decisions has reduced.

In earlier periods, especially between 2023 and 2025, strong demand meant that buyers often had limited time to evaluate options. Properties moved quickly, negotiation margins were low, and delays in decision-making could result in missed opportunities. That environment has now changed.

With demand slowing, buyers have more space to assess projects, compare locations, and negotiate with developers. This does not mean that prices have become low, but it does mean that the terms of the deal can be more flexible.

For end-users who are buying a home for long-term use, this can be an advantage. The ability to take time, verify documents, and negotiate better terms reduces the risk of making rushed decisions.

For investors, however, the situation is more complex. The expectation of quick appreciation is less reliable in a slower market. While long-term fundamentals remain intact, short-term gains may not be as strong as in previous years. This makes entry timing and property selection more important.

There is also a category of buyers who are waiting for a significant price drop. This expectation needs to be evaluated carefully. Historically, Chennai has shown price stability rather than sharp corrections. Even during periods of reduced demand, prices tend to remain steady or grow at a slower pace rather than decline sharply.

The current data supports this pattern. Despite a noticeable drop in sales, prices have continued to increase. This suggests that waiting solely for a price crash may not lead to the expected outcome.

This is the most important question, and it cannot be answered with a single general rule. The decision depends more on individual financial conditions than on market timing.

For buyers with stable income, long-term plans, and a clear requirement, the current market can be suitable. The reduced competition and improved negotiation scope create a more controlled buying environment. The risk of overpaying due to urgency is lower.

On the other hand, buyers who are uncertain about their financial stability or are entering the market purely for short-term gains should be cautious. A slower market can extend the time required to see returns, and holding costs may become a factor.

It is also important to avoid making decisions based on speculation. Trying to predict exact market bottoms is rarely effective. Real estate cycles do not behave in a way that allows precise timing for individual buyers.

A more practical approach is to evaluate whether the property meets long-term needs and whether the financial commitment is sustainable.

In a slower market, strategy matters more than timing. Buyers who approach the process with a clear plan are more likely to benefit from the current conditions.

The Chennai real estate market in 2026 is not experiencing a decline in value. It is adjusting to a set of external pressures that have slowed down transaction activity without significantly affecting price levels.

Sales have reduced, inventory has increased, and buyer sentiment has become cautious. At the same time, developers are maintaining price levels due to cost structures and long-term expectations.

For homebuyers, this creates a more balanced environment. Decisions can be made with less urgency and more analysis. The key is to focus on financial readiness, property suitability, and long-term objectives rather than short-term market movements.

A slowdown does not automatically create risk. In many cases, it creates an opportunity to make better decisions.